| 塑料薄膜: BOPP | CPP | BOPET | BOPA | 胶带产业: 胶带膜 | 丙烯酸及酯| VIP 专区 | 彩印专区: 新闻 | 技术 | 分析 | 行情 | 政策 | 国际频道 |

| 塑料原料: PE | EVA | PP | 粉料 | 溶剂油墨: 醇类 | 芳烃 | 酮类 | 醋酸及酯 | 软包基材: 双拉 | 流延 | 镀铝 | 吹膜 | 阻隔 | 原油专区 |

Europe’s Flexible Packaging Market contracts by 3% in value terms, despite an increase in volume

Rising raw material costs are expected to augment the value of Europe’s flexible packaging market, following declines in 2009.

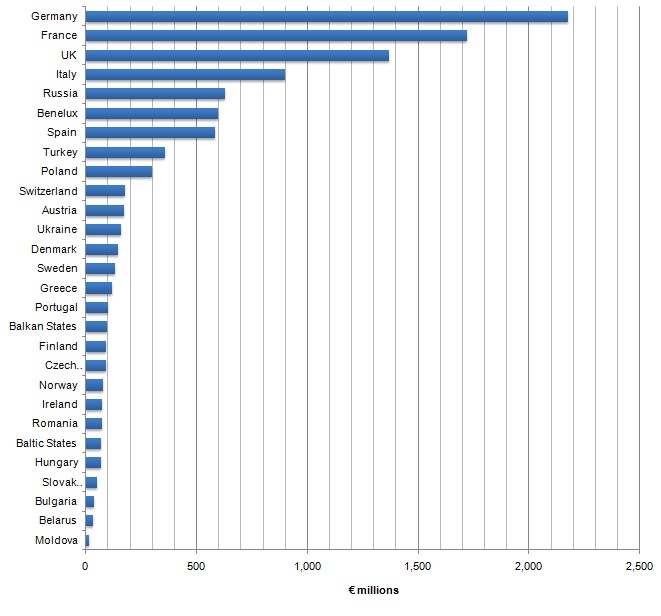

Europe’s converted flexible packaging market declined by 3% in value terms to around €10.4 billion in 2009, equivalent to 44.2 billion m² of materials, according to a report from leading consultancy PCI Films Consulting Ltd. The decline in sales value was primarily associated with the fall in raw material costs, especially in the first half of the year, which was reflected in lower prices to customers. Contrary to some expectations, however, demand in area terms actually increased, albeit by a marginal 1%, as a result of real growth in a number of end use markets in both Western and Eastern Europe.

Commenting on the publication, study author Paul Gaster says: “The robustness of flexible packaging demand is to a great extent underpinned by the strong recession-resistant nature of its end use markets, especially food, pharmaceuticals and pet food, which between them account for around 90% of total European flexible packaging demand. However, raw material costs have risen very strongly this year, reversing the declines in 2009, and this is again putting greater pressure on converter margins.”

One of the major events of the last year has been Amcor completing its acquisition of certain parts of Alcan Packaging, which sees Amcor emerging as by far the largest flexible packaging converter in Europe with approaching 25% overall market share. At the same time a number of other European top ten converters have not yet achieved the critical mass at which they can most effectively challenge the newly enlarged Amcor.